Survey: The Scandinavian subscription market (and what you can learn from it)

Published: December 5, 2024

Denmark, Norway and Sweden are some of the leading European countries when it comes to innovative subscription and membership business models. So, what does the Scandinavian subscription market teach businesses when it comes to customer preferences and habits?

Together with consulting company Subscrybe and payment solution Vipps MobilePay, Billwerk+ surveyed Scandinavian customers from Denmark, Norway and Sweden to find out more about their subscription behaviors, spending and opinions.

Download the PDF summary here.

{kind=link}

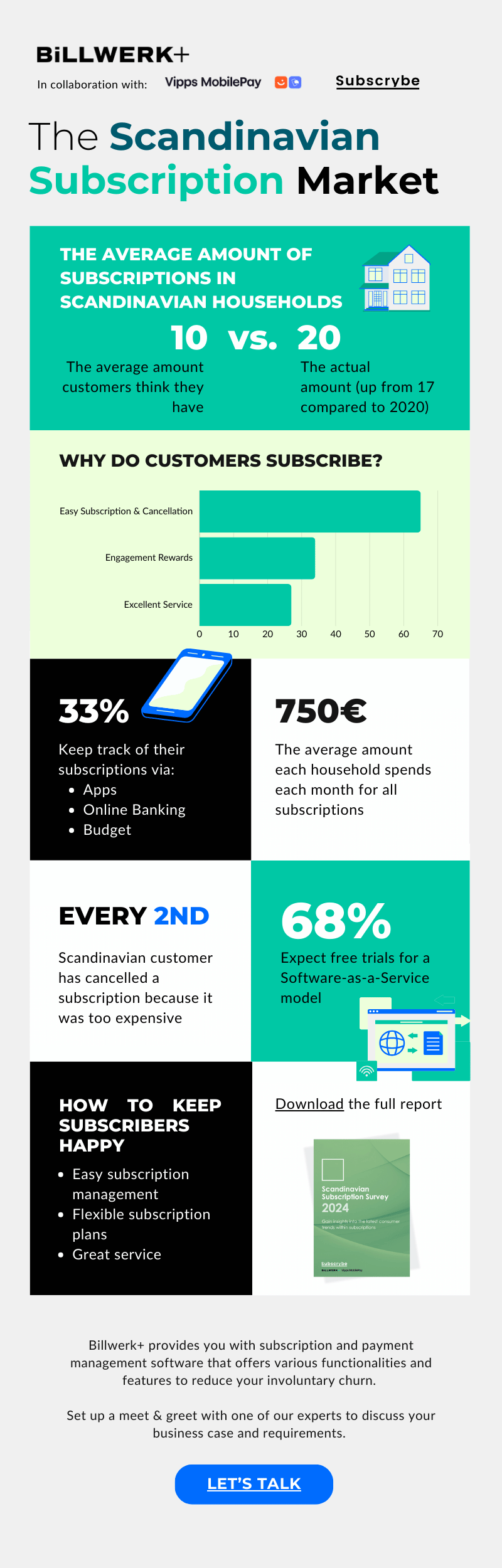

6 Learnings from the Scandinavian subscription market

Customers don’t necessarily want more subscriptions

According to the survey, around 55% of customers do not think that they will increase the number of subscriptions in the future. 19% consider getting more subscriptions and 17% want to reduce the number of subscriptions in the future.

For subscription providers in heavily saturated markets, this means that acquisition might become more difficult and that the real focus should be on retention.

Streaming is popular

When it comes to the big players, streaming is the most popular subscription type, customers subscribe to, with 45% having subscribed to at least 3 streaming services.

However, this doesn’t mean that it will be easy to gain or keep streaming customers. The global competition is massive and “subscription fatigue” is a real phenomenon that keeps customers on the lookout for cheaper and more consolidated services that provide more value.

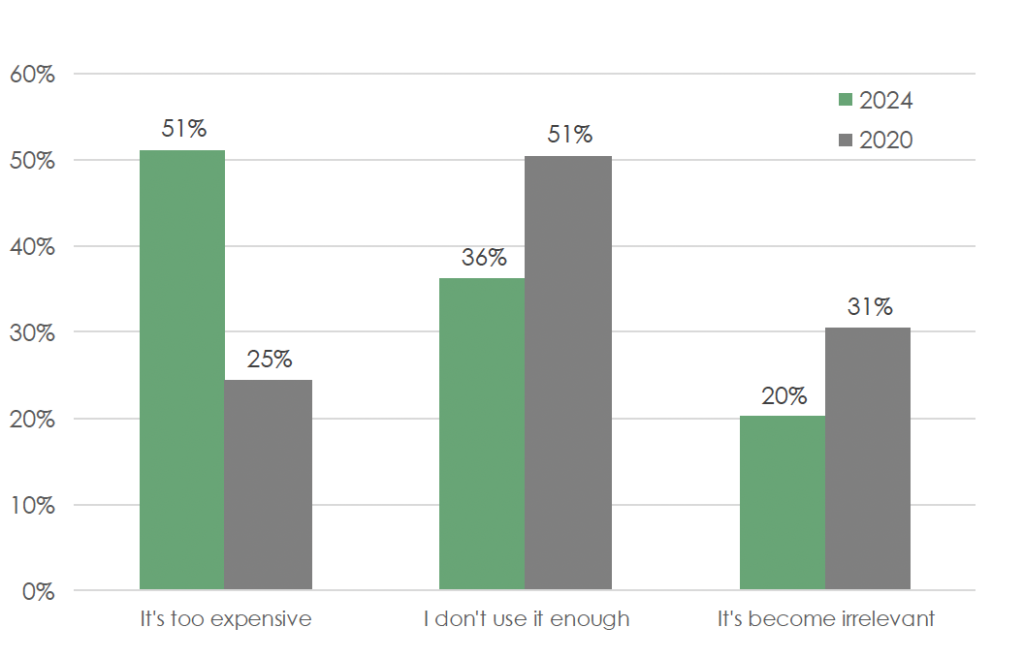

Customers are more price sensitive

Speaking of which: the price has become the biggest reason to unsubscribe. In fact, only 4 years ago, the most important decision-factor to cancel a subscription was “I don’t use it enough”. It’s safe to assume that price increases, the rising number of subscriptions per household and the global competition have created a higher focus on price.

(Reasons, why customers unsubscribe according to the Scandinavian Subscription Market Report)

However, “expensive” does not necessarily mean that the subscription itself is too pricey but that it’s perceived value has decreased.

The common phenomenon of “affective devaluation” occurs when customers are less satisfied with a product, service or reward once they are getting used to it. What once was state of the art is now considered a standard. This can increase if there’s more competition with services and products that seem “new” and therefore more desirable to the “known”.

It’s up to you to either add more value or provide your subscribers with means to gain and see more value (e.g., via new content, new features training material, hacks, best practices, etc.).

There’s also something to be said about many subscription services rewarding new customers with discounts and free trials, whereas loyal customers often don’t see any advantages for their loyalty.

Many companies have created a culture where it’s more cost-saving for customers to cancel and look for sign-up discounts instead of staying subscribed. As mentioned before, with retention being the key metric for long-term success, companies have to find ways to keep loyal subscribers.

By the way, it might seem counter-productive but making it easier for customers to pause their subscription and test out other offers, might have positive long-term effects. It’s not unusual for streaming customers to switch between services throughout the year, depending on new releases.

Flexibility & self-service are key

On average, 40% of survey participants have an idea of their subscription spend and one third keep track of it via app, online bank or budget. The average Scandinavian household spends about 750€ on subscription products per month

When asked, most customers guessed that they had about 10 subscriptions which is about half of the actual amount.

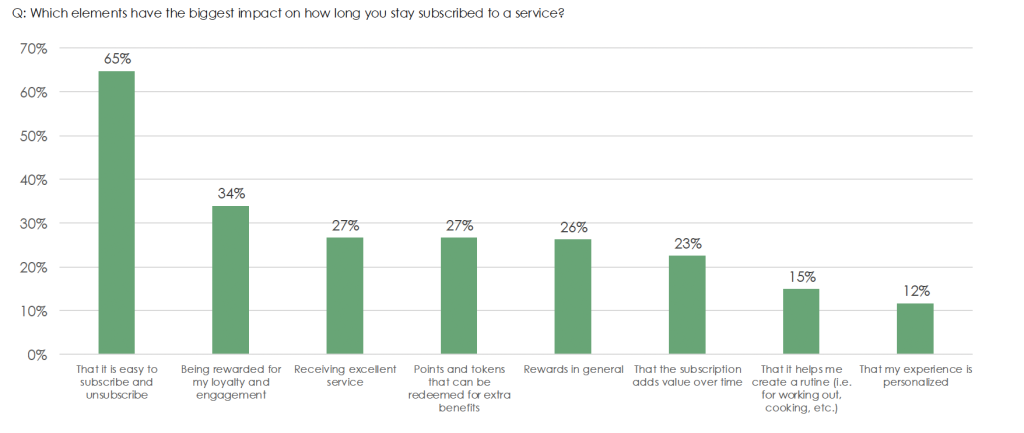

65% of all respondents subscribe to a product or service because it’s easy to subscribe and unsubscribe. The second-most important subscription reason are loyalty rewards (34%).

It seems clear that subscription companies need to make sure to provide easy and transparent ways to manage, pause, and cancel subscriptions, so customers don’t feel “trapped” when signing up or loose overview of their subscription plans.

Furthermore, 86% of Scandinavians prefer a monthly subscription over an annual subscription, even though many annual subscriptions come at a higher discount. Likewise, 68% of customers deem free trial periods as important or very important, underscoring that flexibility is a huge decision marker.

Read in this article, why and when free trials can increase your acquisition and what effect they have on conversion rates.

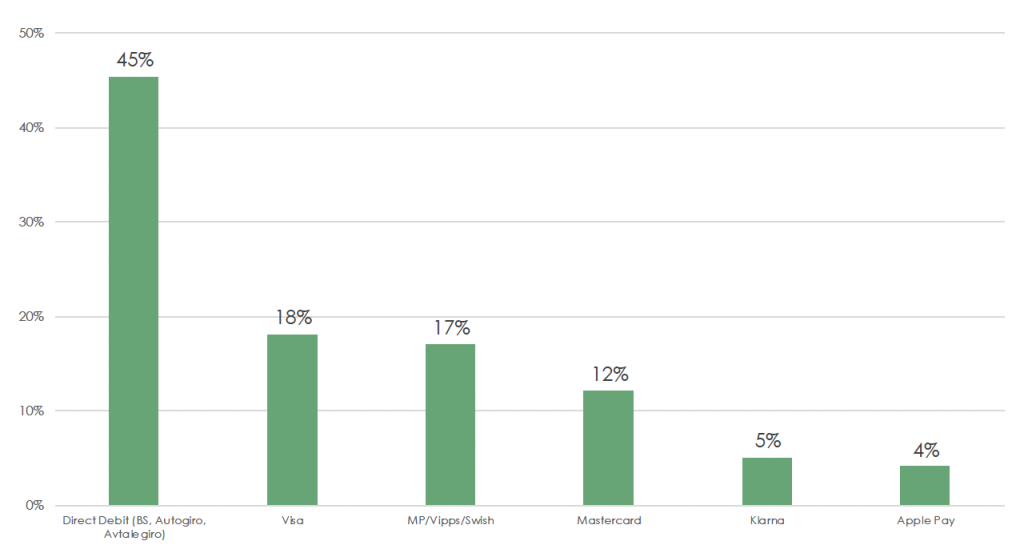

Debit/Bank payments trump credit cards

Even though Scandinavia is a lot more digital than other European markets (such as Germany, for example), many customers still prefer to pay via debit card over credit cards such as Visa or Mastercard. However, credit card payments have increased over the last years, emphasizing a shift in payment behavior (click here for a more extensive overview of payment methods in the nordics).

(Preferred payment methods)

Additionally, preferred payment methods can vary widely depending on the country, customer base and service. Survey your own customer base to identify the right payment method for your subscription plans, since a slight change to a popular payment method can have a huge impact on checkout conversions.

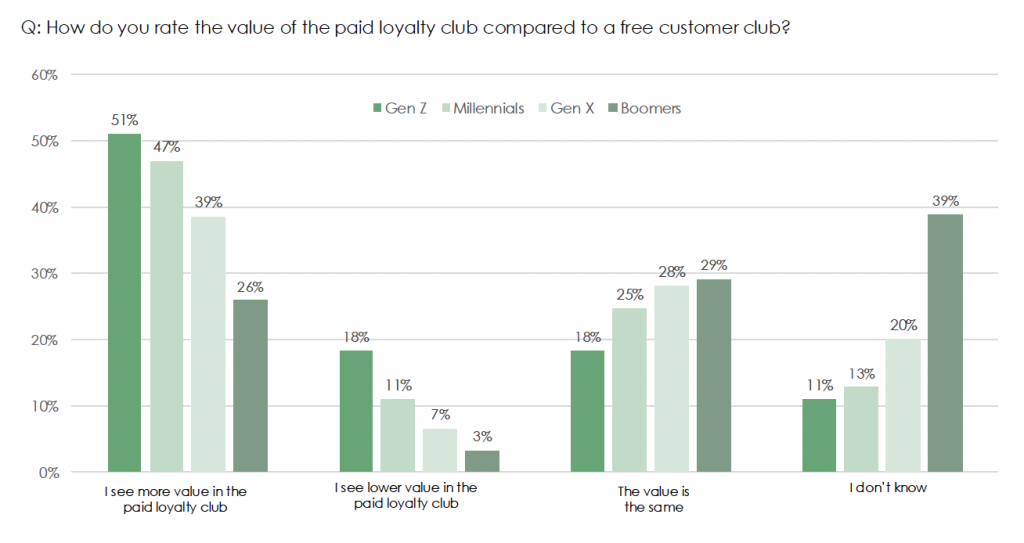

Paid membership programs have potential

Paid membership programs are surprisingly popular, especially among the younger populace. Every second Gen Z sees more value in paid loyalty clubs, followed by Millennials (47%), Gen X (39%) and Boomers (26%).

One could deduct that “Boomers” are just not the right target group for paid membership programs but as with many things in life, there are other reasons that can play into their reluctance:

- Often, loyalty programs and memberships are app-based which might deter customers who do not use their smartphones as often

- Paid programs might be offered predominantly by brands who target younger customers which then creates a chicken/egg-problem: if brands and services that are more popular with Boomers don’t offer paid memberships, then of course, Boomers don’t see the value in them

- Boomers might expect differnet values from membership programs than younger generations, who tend to react very positively to personalized experience. Other incentives might create a higher acceptance rate.

Summary: Flexibility and perceived value drive subscriptions

At the end of the day, what customers most want are flexibility and quality. They want to be free in their decision to subscribe and unsubscribe and they want a product or service that is worth the price.

It’s up to the subscription company to make sure that this worth or value has longevity because the competition is fierce. Customers have more choices and options than ever to cancel and switch. A good relationship, where the customer feels like they get the best out of their subscription.

Learnings:

- An easy cancellation or pause can have a positive impact on conversions

- Monthly payments are more popular among (B2C) customers

- Perceived value (aka, a price that is not deemed “expensive”) is the number one reason for subscriptions (and cancellations)

- Price increases need to be coupled with value-led campaigns (e.g., new features, more flexibility or better user content)

Billwerk+ is your one-stop-shop for payments, recurring billing and subscription management. Sign up for free to see how many options you have to optimize the subscription journey with Billwerk+.

Or book a demo to meet one of our experts, talk about your business case and get a guided tour through our platform.