Studie: Der skandinavische Subscription-Markt (und was wir von ihm lernen können)

Veröffentlicht: Dezember 5, 2024

Dänemark, Norwegen und Schweden gehören zu den führenden Ländern, wenn es um Abo- und Clubmitgliedschaften als Geschäftsmodelle geht. Was kann uns also der skandinavische Abo-Markt über Kundenpräferenzen und Kundenverhalten sagen?

Zusammen mit dem Beratungsunternehmen Subscrybe und dem Zahlungsanbieter Vipps MobilePay hat Billwerk+ skandinavische Kunden aus Dänemark, Norwegen und Schweden befragt, um mehr über ihre Beziehung, Zahlungsvorlieben und Meinungen zu Abonnements und Subscription-Modellen zu erfahren.

6 Best Practices aus dem skandinavischen Subscription-Markt

Kunden wollten nicht unbedingt mehr Abos abschließen

Der Umfrage zufolge wollen 55% der Kunden in der Zukunft keine weiteren Abos abschließen. 19% schließen es nicht aus und 17% wollen die Anzahl der Abonnements eher reduzieren.

Gerade für Subscription-Unternehmen in Märkten mit hohem Wettbewerb kann dies bedeuten, dass die Kundengewinnung schwieriger wird. Ein Fokus auf die Kundenbindung steigt damit an Bedeutung.

Streaming ist populär

Bei den großen Abo-Unternehmen ist Streaming am populärsten. 45% der befragten Kunden haben mindestens drei Streaming-Services abonniert.

Das muss jedoch nicht heißen, dass es einfacher wird, Kunden zu gewinnen und zu halten, ganz im Gegenteil. Der globale Wettbewerb ist massiv und gerade beim Medienangebot ist die „Subscription-Müdigkeit“ ein echtes Problem, das Kunden dazu bewegt, aktiv nach günstigen und umfassenderen Services zu suchen, die Mehrwerte bieten.

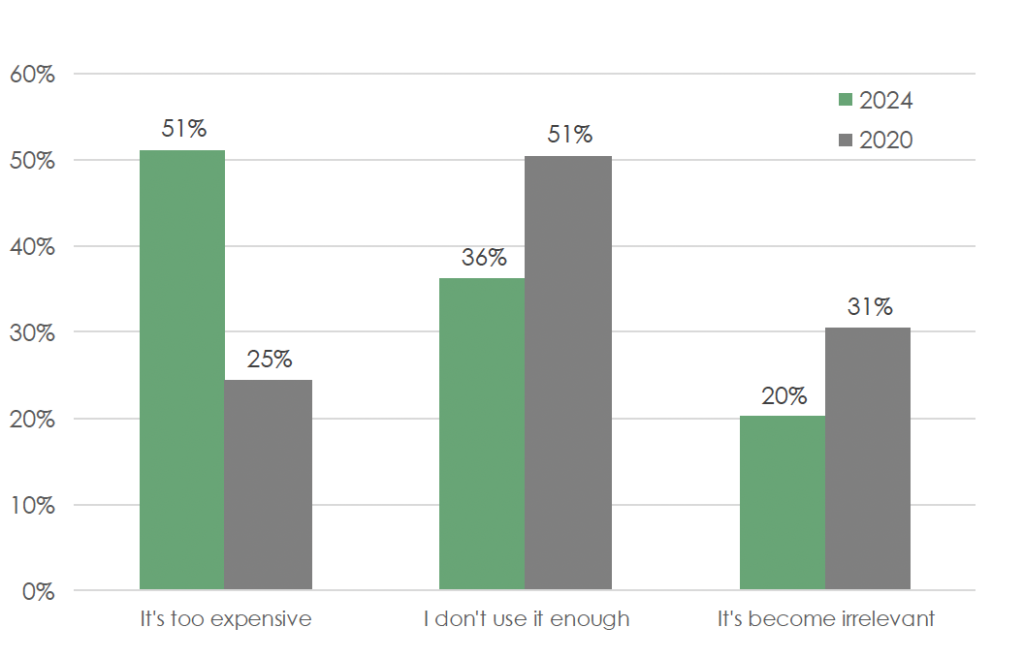

Kunden achten mehr auf den Preis

Ein zu hoher Abo-Preis ist tatsächlich der Hauptgrund, warum Kunden ein Abo kündigen. Das war bei unserer Befragung vor vier Jahren noch etwas anders. Damals nahm die „unzureichende Nutzung“ den ersten Platz ein.

Woran liegt’s?

Wahrscheinlich sorgt die Kombination aus zahlreichen Preiserhöhungen, steigenden Abonnements im Haushalt sowie eine große Auswahl an Abo-Services weltweit dafür, dass der Preis oft den Ausschlag gibt.

(Gründe, warum Kunden ein Abo kündigen, Scandinavian Subscription Market Report, 2024)

Doch ein hoher Preis muss nicht immer bedeuten, dass das Abo selbst zu teuer ist. Es signalisiert lediglich, dass der Kunde den Wert des Abonnements geringer als den Preis einstuft.

Eine größere Rolle kann dabei ein Phänomen spielen, dass in der Konsumentenpsychologie auch als „Affektive Devaluierung“ bezeichnet wird. Je länger Kunden ein Produkt, einen Service oder eine Belohnung nutzen, desto mehr wandelt sich dessen Besonderheit in eine Selbstverständlichkeit. Was vor einiger Zeit noch State-of-the-Art war, ist plötzlich ein Standard, der – um es mal salopp zu formulieren – niemandem mehr vom Hocker reißt.

Dieses Gefühl wird verstärkt, wenn die Konkurrenz Produkte und Services anbietet, die neu und frisch wirken. Gerade im Produkt- und Medienbereich ist das oft der Fall, weil das Angebot anderer Anbieter eine Abwechslung bietet.

Für Sie als Unternehmen gilt es also, dass Ihre Abonnenten den Wert ihres Abos nicht nur kennen, sondern immer neu kennenlernen, indem Sie neue Produkte entwickeln, Content zur kreativen oder professionellen Nutzung teilen oder anderweitig das Nutzererlebnis ausbauen.

Es sollte auch nicht unerwähnt bleiben, dass viele Abo-Services ihre Neukunden oft mit Rabatten und kostenlosen Probe-Abos belohnen, während loyale Kunden selten Vorteile wahrnehmen.

Viele Unternehmen haben dadurch eigenständig eine Kultur entwickelt, in der es günstiger für Kunden ist, zu kündigen und sich mit Einstiegsrabatten neu zu registrieren, anstatt einem Abo-Service treu zu bleiben. Wenn Kundenbindung die wichtigste Erfolgsmetrik für Subscription-Unternehmen ist, dann müssen diese Unternehmen anfangen, ihre loyalen Kunden pro-aktiv an sich zu binden.

Übrigens, auch wenn es kontraproduktiv klingt, es kann positive Langzeiteffekte haben, Kunden das Pausieren von Abos zu erleichtern. Bei Streaming-Kunden ist es beispielsweise nicht ungewöhnlich, dass sie im Jahr zwischen verschiedenen Services wechseln, je nachdem, welche Serien, Filme und andere Inhalte gerade frisch veröffentlicht wurden.

Flexibilität und Self-Service sind Erfolgsgaranten

Im Durchschnitt wissen ca. 40% aller Umfrageteilnehmer, was sie für Abonnements ausgeben. Ein Drittel trackt alle Abonnements via App, Online-Bank oder das Budget-Management. Ein durchschnittlicher skandinavische Haushalt gibt ungefähr 750€ im Monat für Abo-basierte Services und Produkte aus.

Bei der Befragung haben die meisten Kunden außerdem unterschätzt, wie viele Abonnements sie eigentlich abgeschlossen haben. Während ein Haushalt im Durchschnitt 20 Abos umfasst, haben die meisten Umfrageteilnehmer die Zahl auf 10 geschätzt.

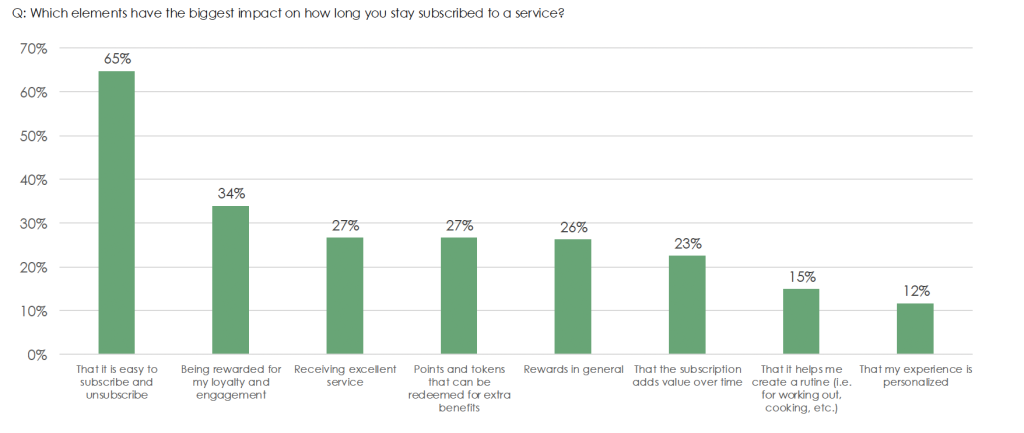

65% aller Kunden haben ein Produkt abonniert, weil es einfach ist, das Abo abzuschließen und zu kündigen. Auf Platz zwei (34%) für Abonnements stehen Belohnungen, was mit der großen Popularität bezahlter Kundenclubs im skandinavischen Raum zusammenhängt.

Das waren jetzt viele Zahlen, die jedoch bestimmte Schlüsse ziehen lassen:

Unternehmen müssen dafür sorgen, dass Kunden die Abos einfach und transparent abschließen, managen, pausieren und kündigen können. Denn selbst beim Abschließen eines Abos schauen Kunden bereits darauf, wie einfach es ist, es wieder zu kündigen. Niemand möchte im Abo „gefangen“ sein.

Zusätzlich bevorzugen 86% aller Skandinavier ein monatliches gegenüber einem jährlichen Abo, obwohl die jährliche Zahlung oft mit signifikanten Rabatten einhergeht. Auch halten 68% der Kunden ein kostenloses Probe-Abo für selbstverständlich. Flexibilität ist also auch dahingehend ein großer Hebel für die Kaufentscheidung.

Lesen Sie in unserem Blogbeitrag, warum und wie kostenlose Probe-Abos ihrer Akquise und Konversionen beeinflussen können.

Debit/Bankzahlungen trumpfen Kreditkarten

Auch wenn Skandinavien sehr viel digitaler ist als manch anderer europäischer Markt (Deutschland, beispielsweise), ziehen viele Kunden dennoch weiterhin die Debitkarte der Kreditkartenzahlung vor. Doch in den letzten Jahren hat sich das Verhältnis zugunsten Kreditkarten stetig verbessert, es ist also ein Wechsel im Zahlungsverhalten zu beobachten.

Zusätzlich sollte immer beachtet werden, dass bevorzugte Zahlungsmethoden stark abhängig vom Land, verschiedener Kundengruppen oder Portfolios ist. Daher lohnt es sich, die eigenen Kunden zu befragen, um die richtigen Zahlungsmethoden für Ihre Abo-Pläne zu identifizieren. Tatsächlich kann ein Wechsel zu einer populären Methode einen großen Einfluss auf Checkout-Konversionen und Umsätze haben.

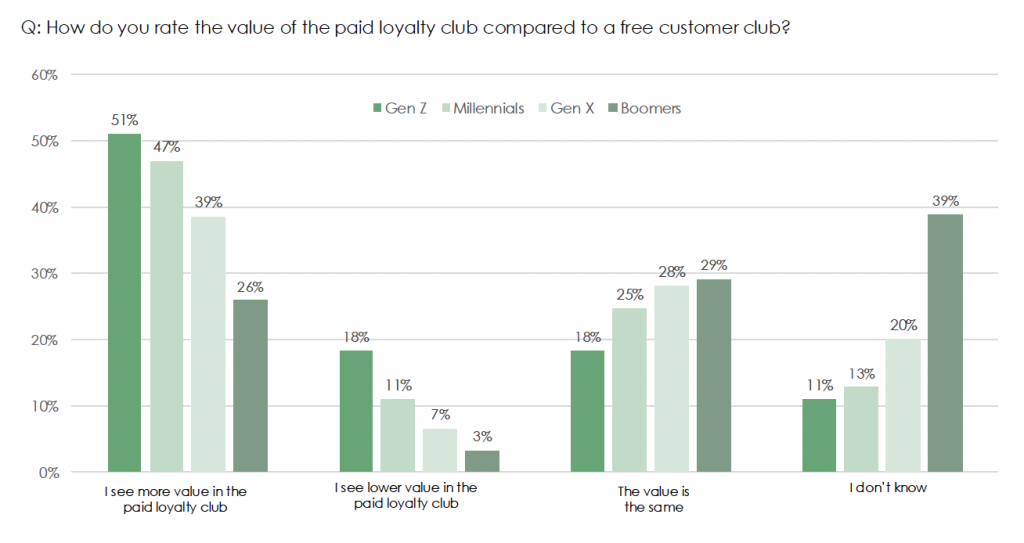

Bezahlte Kundenclubs haben Potenzial

Kundenmitgliedschaften im Bezahl-Abo sind erstaunlich populär in Skandinavien, insbesondere unter jüngeren Menschen. Jeder zweite Gen-Z Kunde sieht einen größeren Mehrwert in Kundenclubs, die etwas kosten, gefolgt von Millennials (47%), Gen X (39%) und Boomer (26%).

Nun könnte man davon ausgehen, dass „Boomer“ einfach nicht die richtige Zielgruppe für bezahlte Kundenclubs sind, doch wie bei so vielen Dingen im Leben können hier auch andere Gründe die Ursache sein:

- Oft sind Loyalitätsprogramme App-basiert, was Kundengruppen abschrecken kann, die ihre Smartphones nicht so intensiv nutzen.

- Eventuell werden viele bezahlte Kundenclubs von Marken angeboten, die eher junge Zielgruppen ansprechen. Es entsteht ein Henne/Ei-Problem. Wenn Boomer wenig bis keine attraktiven Angebote haben, dann werden sie auch keine Mehrwerte darin sehen können.

- Boomer haben potenziell andere Erwartungen an Clubmitgliedschaften. Jüngere Generationen ziehen beispielsweise mehrheitlich personalisierte Angebote vor. Andere Anreize und Vorteile könnten auch die Akzeptanzrate erhöhen.

Zusammengefasst: Flexibilität und der empfundene Wert erhöhen Konversionen

Am Ende des Tages wollen Kunden Flexibilität und Qualität. Sie wollen frei in ihrer Entscheidung sein, ob sie etwas abonnieren oder kündigen und sie wollen ein Produkt mit einem hohen Kosten/Nutzen-Wert.

Es liegt an den Unternehmen, dass Abos und Mitgliedschaften klar kommunizierte und langfristige Mehrwerte haben, denn der Wettbewerb ist unerlässlich. Kunden wollen Optionen, auch, wenn es um Abo-Wechsel und -Kündigungen geht. Eine gute Beziehung ist dabei grundlegend, damit Kunden das Gefühl haben, sie können das Beste aus ihrem Abo herausholen.

Learnings:

- Ein einfacher Kündigungs- oder Pausierungsprozess kann sich positiv auf Konversionen auswirken

- Monatliche Zahlungen sind beliebter unter B2C-Kunden

- Der gefühlte Wert (also ein Preis, der nicht als „teuer“ empfunden wird), gehört zu den Top-Gründen, warum Kunden Abos abschließen oder kündigen

- Preiserhöhungen müssen mit wertegesteuerten Kampagnen einhergehen (z.B. neue Features, mehr Flexibilität, besserer User-Content).

Billwerk+ ist Ihr One-Stop-Shop für Zahlungen, wiederkehrende Rechnungen und Subscription Management. Melden Sie sich jetzt zum kostenlosen Test-Abo an oder buchen Sie einen Demotermin mit unseren Experten, um über Ihren Business Case zu reden.